Routine care and clinical encounters found in medical claims data give underwriters meaningful visibility into early‑life health.

More parents and grandparents are buying life insurance for kids. This impulse could seem morbid at first glance, but it’s actually generous. Buying a policy that early can lock in low rate and guarantee those little ones will have affordable coverage later in life when they grow up and have their own families, regardless of any future medical conditions or impairments. In the case of whole life insurance, accumulating cash value can provide a financial asset that can be accessed for education or other needs.

From the carrier’s perspective, juvenile policies can stay in force for decades, leading to expanded coverage in adulthood. Digital distribution has also made it easier to reach young families. But how should life insurance carriers underwrite these unique risks? Many operate under the incorrect assumption that juvenile applicants simply haven’t had time to generate enough meaningful health data to justify ordering Irix Medical Data or Prescription Data.

Although juvenile profiles usually feature fewer prescription fills than adult profiles, young people typically have regular wellness checks that result in surprisingly robust medical records.

The myth of “thin” juvenile data

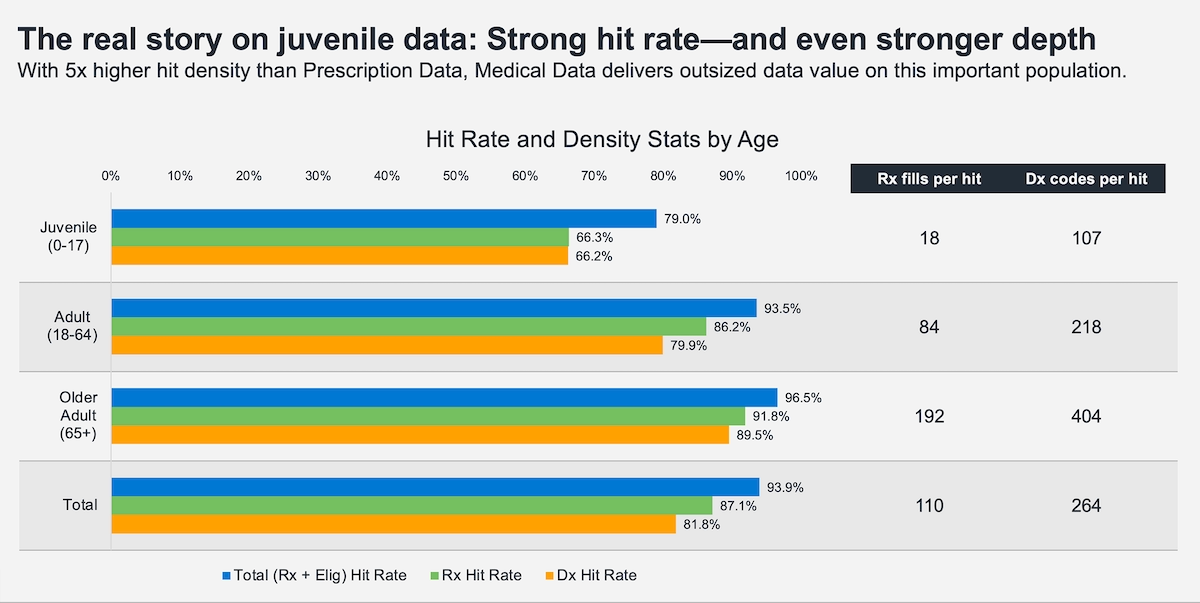

Compared to adults, juveniles have had less time to develop chronic conditions and don’t usually have the hundreds of prescription fills we see in most adult files. However, juvenile data is still more (often, a lot more) robust than many carriers expect. In part, this reflects the fact that children and youths interact with the healthcare system more consistently and more predictably than many adults. Kids have regular wellness-care visits, screenings, and developmental check‑ins that often produce a lot of useful claims data, even if the applicant has never filled a long‑term prescription.

In other words, the absence of chronic illness does not equal the absence of data.

Severity still matters

Serious impairments may indeed be less commonly identified in juveniles. But when they do exist, they matter disproportionately. Conditions such as early‑onset diabetes, hypertension, obesity, fatty liver disease, or significant congenital or developmental issues are not expected in this population—but they do occur, and when they do, the mortality implications are significant.

Relying on Prescription Data alone may present a misleading picture

In juvenile populations, medical codes often outnumber prescription records by a wide margin. For the purposes of comparison, the average adult query yields a roughly 2:1 ratio of medical codes to prescription fills. Meanwhile, queries on juvenile applicants can yield a 5:1 code-to-fill ratio. This simply reflects the fact that when providers see kids, diagnoses, encounters, and clinical observations are frequently captured without ever resulting in a prescription.

Our customers’ experience has proven that both Prescription Data and Medical Data should be foundational in almost any life underwriting situation, but the greater relative significance of medical codes where the youngest applicants are concerned means that inclusion of Medical Data is particularly important when it comes to understanding their mortality risk.

Real carrier experience has shown mortality data isn’t the whole story

Another common objection is the lack of large‑scale mortality data for juveniles. Comprehensive death data is limited simply because juveniles, thankfully, do not die in large numbers. But in the same way that there are good reasons to buy a juvenile policy that have nothing to do with the death benefit, the underwriting of such policies has never been based on mortality alone. The healthcare system is actually very good at documenting early‑life health, and Medical Data helps underwriters think strategically about care patterns and potential future risk.

This isn’t some underwriting-in-a-perfect-world argument. In numerous studies, ordering Medical Data on juveniles turned skeptics into believers by revealing a level of clinical detail they simply didn’t expect to find.

Now, instead of guessing whether the data exists, carriers can evaluate it directly—looking at encounter density, condition categories, and rule incidence across their own blocks of business.

The question is no longer “Is there enough data on juveniles?” but rather “Why wouldn’t we use data that’s already there?